pzbrickey23613

About pzbrickey23613

Understanding Personal Loans with Dangerous Credit: A Complete Examine

Introduction

In in the present day’s monetary landscape, personal loans serve as a crucial useful resource for individuals looking for to handle unexpected expenses, consolidate debt, or finance important purchases. However, for these with dangerous credit score, accessing these loans might be particularly difficult. This report delves into the intricacies of personal loans for people with dangerous credit, inspecting the sorts of loans available, the implications of unhealthy credit score on loan eligibility, and methods for improving creditworthiness.

Defining Dangerous Credit

Credit score scores, which usually vary from 300 to 850, are a numerical representation of a person’s creditworthiness. A credit score rating under 580 is usually thought of ”dangerous” credit score. Components contributing to a low credit score score embody missed payments, excessive bank card balances, bankruptcy, and defaulted loans. Understanding the implications of dangerous credit is important for borrowers looking for personal loans, as lenders usually understand them as high-threat shoppers, resulting in higher curiosity rates or outright denial of loan functions.

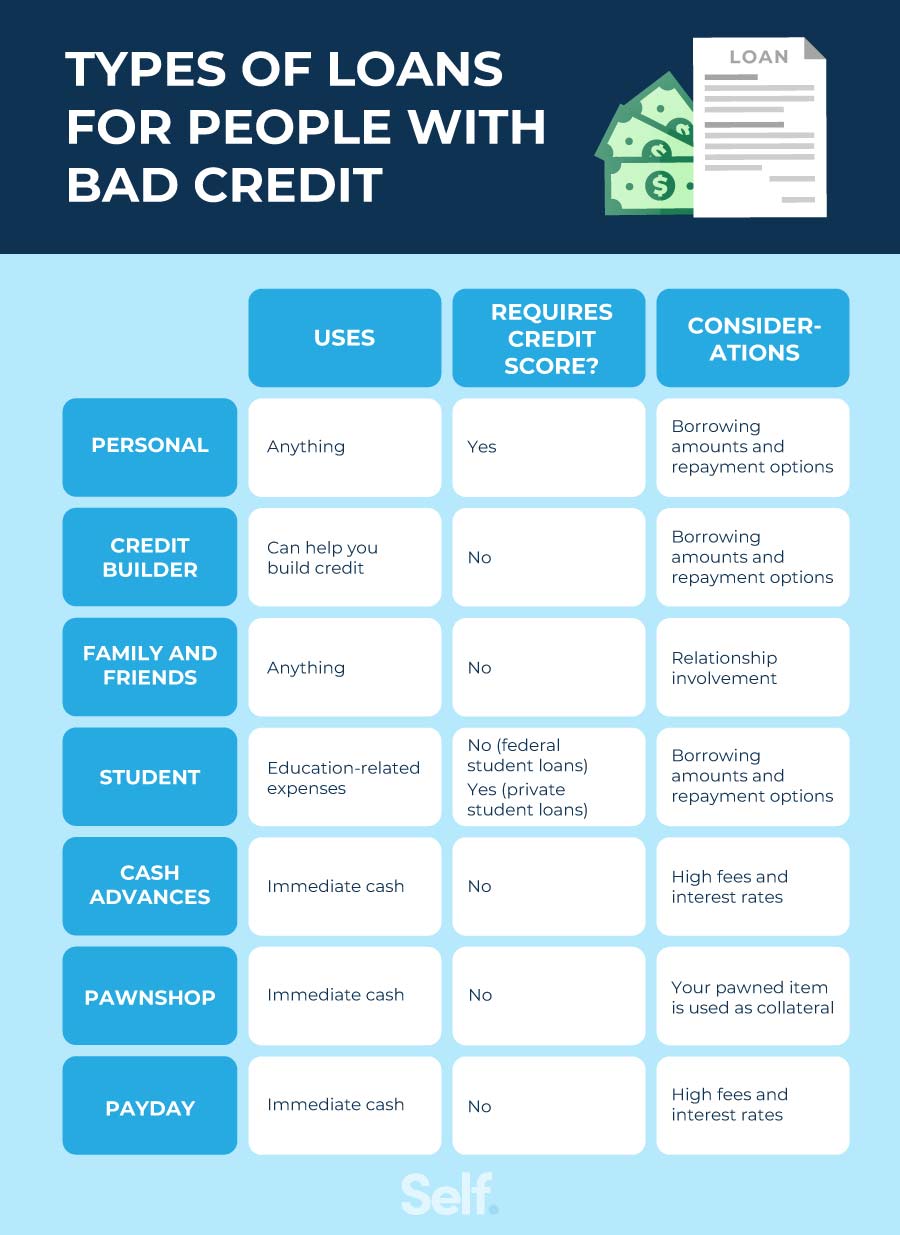

Forms of Personal Loans Accessible for Bad Credit score

- Secured Personal Loans: These loans require collateral, reminiscent of a automotive or financial savings account, which reduces the lender’s danger. If the borrower defaults, the lender can seize the collateral. Secured loans typically have lower interest rates than unsecured loans, making them a viable choice for individuals with dangerous credit.

- Unsecured Personal Loans: These loans do not require collateral, however they usually include higher interest rates and stricter eligibility criteria. Lenders assess the borrower’s creditworthiness primarily through their credit score score and revenue. People with dangerous credit could find it challenging to qualify for these loans.

- Peer-to-Peer (P2P) Lending: P2P platforms join borrowers with individual lenders keen to fund loans. Whereas some P2P lenders could consider borrowers with dangerous credit, curiosity rates can be steep. Borrowers should carefully overview the phrases before proceeding.

- Credit Union Loans: Credit score unions typically have more flexible lending standards than traditional banks. Members with bad credit could find it simpler to secure a personal loan by way of a credit union. Moreover, credit unions typically supply lower curiosity charges and fees in comparison with other lenders.

- Payday Loans: Whereas these quick-time period loans could also be accessible to those with unhealthy credit score, they come with exorbitant curiosity rates and charges, resulting in a cycle of debt that may be troublesome to flee. Borrowers should method payday loans with warning.

Impact of Unhealthy Credit on Loan Eligibility

Unhealthy credit considerably impacts loan eligibility. Lenders assess danger based on credit scores, and a low score often leads to increased curiosity charges or loan denials. Factors that lenders consider include:

- Credit score Historical past: A history of late funds or defaults raises pink flags for lenders.

- Debt-to-Revenue Ratio (DTI): A excessive DTI indicates that a borrower might battle to make funds, influencing lender selections.

- Employment Stability: Lenders prefer borrowers with stable employment, as it suggests a dependable revenue supply for loan repayment.

Strategies for Enhancing Creditworthiness

For individuals with bad credit score in search of personal loans, enhancing creditworthiness is essential. Here are a number of methods to think about:

- Assessment Credit score Reports: Often checking credit experiences for errors may help people determine and dispute inaccuracies that may be negatively impacting their scores.

- Pay Payments on Time: Constantly making payments on time is one in every of the best methods to improve credit scores. Establishing computerized funds or reminders can assist guarantee well timed payments.

- Reduce Debt: Paying down present debts can enhance credit utilization ratios, which positively affects credit score scores. Prioritizing high-curiosity debts may save money in the long term.

- Limit New Credit Purposes: Every credit inquiry can barely decrease a credit score. Limiting new applications may also help maintain a healthier credit profile.

- Consider a Secured Bank card: Secured credit cards require a money deposit as collateral and can help rebuild credit when used responsibly.

Finding the best Lender

When looking for personal loans with bad credit score, it is crucial to shop round for lenders who specialize in excessive-threat borrowers. Online platforms and local credit score unions could offer more favorable terms than traditional banks. Borrowers should carefully evaluate loan terms, together with interest charges, charges, and repayment schedules, to ensure they select the very best possibility for their monetary scenario.

Conclusion

Securing a personal loan with unhealthy credit can be challenging, but it’s not not possible. By understanding the varieties of loans out there, the implications of unhealthy credit on eligibility, and methods for improving creditworthiness, people can navigate the lending panorama more effectively. If you have any thoughts regarding wherever and how to use personal loans for bad credit houston, you can get in touch with us at the site. It’s important to strategy borrowing with warning, guaranteeing that the chosen loan aligns with one’s financial targets and repayment capabilities. Ultimately, enhancing one’s credit score score can lead to raised loan choices and extra favorable terms in the future.

No listing found.